Menu

If you’ve been with us for a while, you’ve likely heard us emphasize the value of building diversified portfolios. The first half of this year has provided us with a compelling reminder of why it matters.

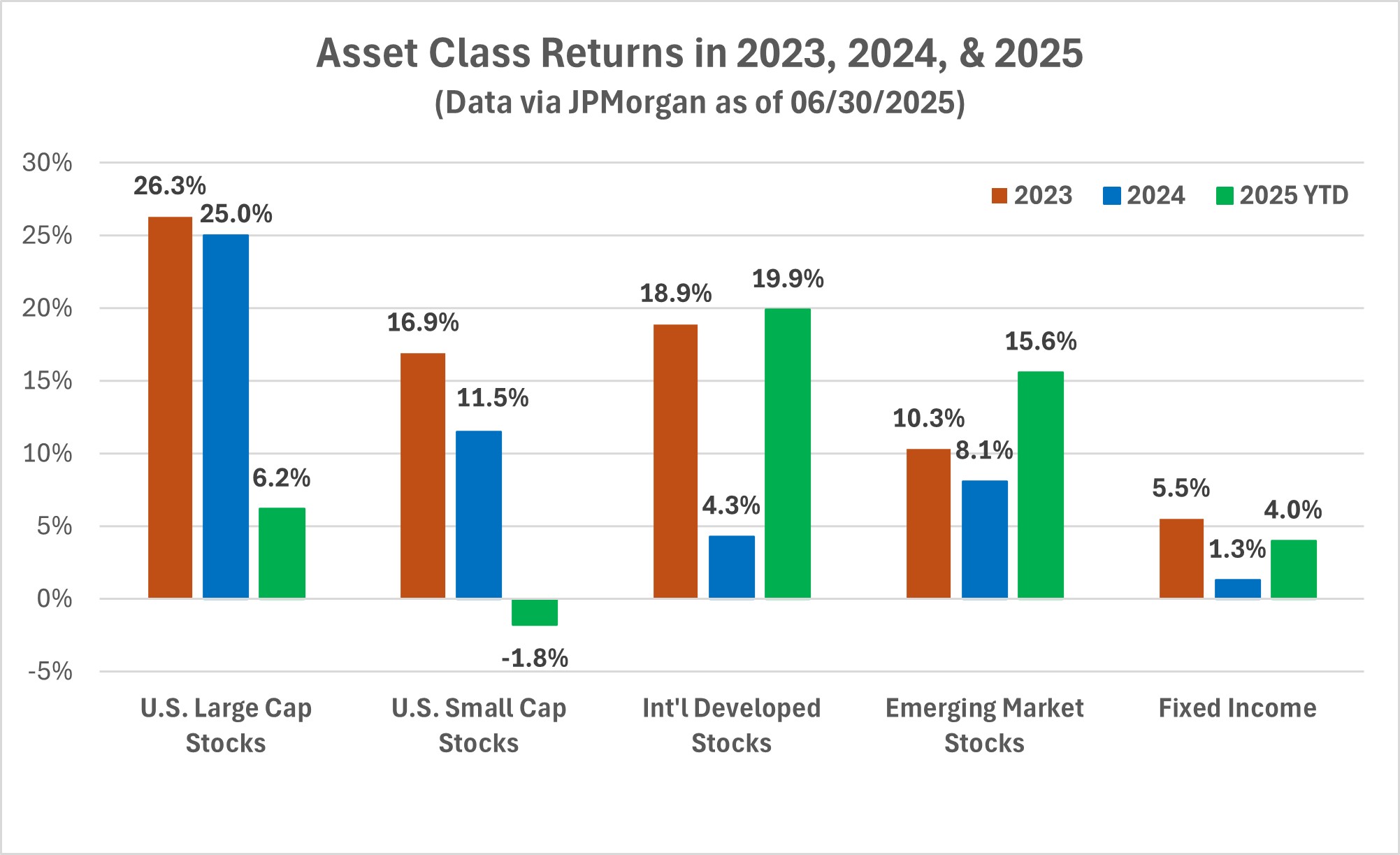

The chart below illustrates year-to-date returns across a range of asset classes through the end of June, and it compares those with respective returns in 2023 and 2024.1 For example, U.S. small-cap stocks have struggled so far in 2025, down nearly 2%. Meanwhile, international developed market stocks have quietly led the pack with gains nearing 20% on the back of economic revitalization efforts in member states of the European Union and early signs of a pro-investment regulatory environment developing there.2 Emerging market stocks are also up double digits in 2025. This has been in sharp contrast to the recent past, when a strong U.S. dollar and the notion of “American exceptionalism” led U.S. stocks to dominate the investment landscape and global diversification felt less rewarding.3

This kind of performance dispersion is exactly what diversified portfolios are designed to capture. In years like 2022 – when most stocks and bonds were down, and there was a lot of chatter about the “death of the 60-40 classic asset mix”4 – the benefits of having a diversified portfolio appear muted. It takes years like 2025, when leadership shifts, to realize the payoff.

This is true of non-traditional investment assets as well. Gold, used as an alternative or inflation hedge in many client portfolios, was up more than 25% through the first half of 2025.5 Performance like this underscores the value of including non-equity investment assets in select portfolios.

We’ve never met anyone able to reliably predict when or where market leadership will rotate. For this reason, we build client portfolios that are globally diversified to ensure we’re not relying on a single region, asset class, or theme to carry the weight. We have always been firm believers in the value of diversification, even if it fell out of popularity for a period of time.6

Our entire team at Sapient is grateful for the opportunity to serve you.

Sources:

1. JPMorgan “Guide to the Markets: Q2 2025,” June30, 2025: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

2. Capital Group RIA Insider, “New Catalysts SpurInternational Stocks,” June 23, 2025: https://www.capitalgroup.com/ria/insights/articles/new-catalysts-spur-international-stocks.html

3. First Eagle,”Non-US Equities: An Exception toAmerican Exceptionalism?”, June 23, 2025: https://www.firsteagle.com/insights/non-us-equities-exception-american-exceptionalism

4. Rosenberg Research, “Early Morning with Dave,”July 7, 2025: https://www.earlymorningwithdave.com/archive

5. Morningstar Direct: net return of iShares GoldTrust (symbol: IAU) and its related index, LBMA Gold Price PM index, for the period 01/01/2025 - 06/30/2025.

6. AQR, “International Diversification – Still NotCrazy After All These Years,” May 3, 2023: https://www.aqr.com/Insights/Research/Journal-Article/International-Diversification-Still-Not-Crazy-after-All-These-Years

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitute the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Indexes used for the Asset Class Returns Chart are as follows: U.S. Large Cap: S&P 500, U.S. SmallCap: Russell 2000, Int’l Developed Stocks: MSCI EAFE, Emerging Market Stocks: MSCI EME, and Fixed Income: Bloomberg U.S. Aggregate. Past performance and yields are not indicative of future results. Investors cannot invest directly in an index.