Menu

The year 2021 continues to bring with it market surprises and an above-average ebb and flow of market and economic uncertainty. We recognize the challenge in discerning truly meaningful signals amidst all the noise from financial news, and we believe the three Q&A topics below are important and timely for our clients:

Rising inflation has been all over the financial news in recent months, and for good reason – the 12-month percentage change in the U.S. Consumer Price Index (CPI) for April, May, June, and July ranged from 4.2% to 5.4% and were the highest readings in more than a decade.[1] Add to the mix stories about rising commodity prices like oil and lumber this spring,[2] as well as used car and truck prices through the summer,[3] and it’s no surprise markets and media started paying close attention. Sustained levels of high inflation are important to consumers concerned about rising prices at the register, and they’re important to investors concerned about the potential impact on portfolios. After all, very high levels of inflation have historically been value-destructive for both stock and bond markets.[4]

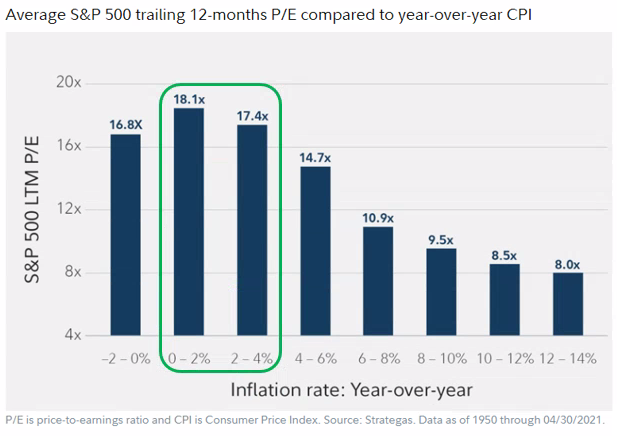

Markets largely anticipated and priced in this higher level of inflation through the late spring and summer months,[5] recognizing how significantly more open our economy is than it was in mid-2020. A more nuanced debate about inflation has been about whether this higher level is a short-term trend (aka “transitory”) or a longer-term trend. Although strong opinions can be found on both sides, currently the markets (and a number of experts) expect the 4%-plus inflation readings will be short-lived – more specifically, Treasury bond markets have priced in an expected inflation rate of 3.3% over the next 12 months with a gradual drop to 2.6% for the next five years.[6] That is still higher than the Federal Reserve’s target inflation rate of 2%, but not so much as to be a major concern to financial markets. As illustrated below, inflation rates of 0-2% have historically led to the stock market’s highest valuations, followed closely behind by inflation rates of 2-4%.[6] However, only time will tell whether the market’s inflation predictions are correct. If incorrect, and inflation remains at elevated levels of 4% or higher through the fall, it could have a material negative impact on markets. We tend to agree with the market and will continue to monitor and assess in the coming months.

Yes, we believe higher tax rates are likely within the next year. The specific details are expected to surface during Congress’s Fiscal Year 2022 budget reconciliation process, which is about to get underway. There has been a lot of posturing leading into it, and uncertainty remains regarding the total spending package and accompanying taxes and/or cuts to help fund it. That said, the starting points for negotiation in the August 9th budget release were $3.5tn in new spending with an accompanying $1.7tn in offsets from new taxes and/or budget cuts.[7] This has the potential to result in a net fiscal spend of 2.5% of GDP, the largest expansion of fiscal policy since Reagan’s first term 40 years ago.[8] However, the imminent debt ceiling negotiations and next year’s mid-term elections may temper even some Democratic party members’ willingness to spend or tax at levels this high. Blending expectations from multiple research partners, we believe the most likely tax increases could include an increase in (1) the corporate tax rate from 21% to 25%, (2) the GILTI (multinational corporate) tax rate from 10.5% to 18%, (3) capital gains and dividend tax rates from 20% to 28%, and (4) the top marginal income tax rate from 37% to 39.6%. All of these will likely be effective for calendar year 2022, with the exception of capital gains tax rates which could possibly be retroactive to include the final 3-4 months of this year.[8] None of these expected tax changes are dramatic enough to shift how Sapient builds investment portfolios at the highest level. Instead, they further emphasize the value in our approach to customizing clients’ portfolios across taxable vs non-taxable accounts to enhance after-tax portfolio outcomes.

Through the end of July, the MSCI EM (Emerging Market) Index of stocks was only up 0.3% for the year. This muted performance was largely driven by the MSCI China Index’s decline of -12.3% for the year, as China now represents more than one-third of the EM Index.[9] Some of the market sell-off in China has been linked to rising COVID-19 cases in the region,[10] but arguably the leading cause has been heightened regulatory policies and oversight by the Chinese government, particularly for its largest technology and for-profit education companies that trade on overseas exchanges.[11] China’s expressed intent with these policy changes is to further develop and improve the quality of their capital markets infrastructure through both judicial and legislative reform and enforcements, helping address important issues like judicial process and fraud enforcement.[12] In the short-term this has negatively impacted those markets and we believe market risks could remain heightened between now and year-end, particularly if COVID-19 cases continue to rise in China and neighboring countries, but we believe these structural market reforms may ultimately prove beneficial to China and EM investors in the intermediate to long-term. So we’re short-term cautious, long-term bullish on EM stocks and are rebalancing clients’ EM exposures back to target as appropriate.

Thank you for allowing us to serve you and steward your investment capital with great care.

Sources:

1. https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm

3. Broadridge, “Should You Be Concerned About Inflation?,” July 2021

6. https://institutional.fidelity.com/app/item/RD_9895518.html

8. Strategas, “Policy Outlook,” August 10, 2021

9. Data Source: Morningstar Direct

12. Morgan Stanley Wealth Management, “On the Markets,” August 2021

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitutes the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Past performance is not a guarantee of future results. Indexes, such as the MSCI Emerging Markets Index, are not directly investable.