Menu

Russia’s full-scale invasion of Ukraine has been characterized as one of the most intense military conflicts on the European continent since World War II.[1] The first order effects of this conflict become clearer each day – namely, significant loss of lives and economic depression for both the Ukraine and Russia, along with rising energy and food prices for Europe and other parts of the world. However, second order effects are still unclear – how much will this impact other global economies and geopolitics in the coming weeks and months? Will it reduce the pace at which the Federal Reserve hikes rates? Will it increase or decrease China’s appetite to invade Taiwan? Could it catalyze a nuclear agreement between the US and Iran to unlock additional global oil supplies? Meanwhile, third order effects won’t be known for years to come – will this accelerate current trends of de-globalization and re-routing of global supply chains? Will it lead to a resurgence of NATO and foster greater collaboration amongst the world’s developed nations? We believe at least some of these outcomes are more likely than not given the grave and historic nature of this conflict. But it’s too early to be fully confident about any of them.

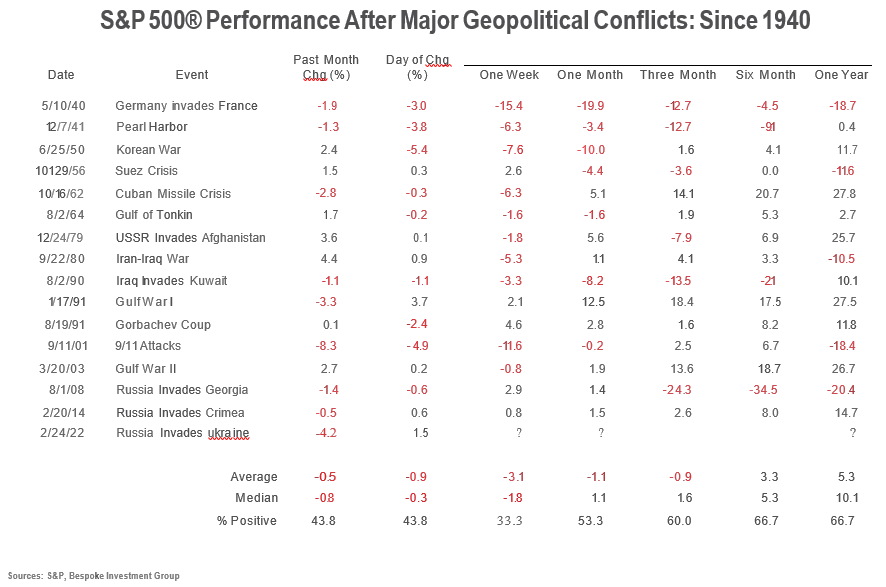

It feels a little callous to talk about investment portfolios in the wake of this crisis, but as fiduciaries and stewards of your capital this is job #1 for us and we would be remiss to not share a brief update. Russia is the 11th largest economy in the world[2] (around 1.3% of global GDP),[3] and exposure to Russian and Ukrainian investments in our clients’ portfolios average less than half of one percent. We have no economic or political prognostications about what Russia will do next or how long this conflict will last, and historical examples to look to as a guide are limited and vulnerable to “this time is different” arguments. However, when we look back at geopolitical conflicts over the past seven decades we find that, in most cases, the S&P 500 has rebounded within three to six months, as illustrated below.[4]

We have not made any significant portfolio changes at this time. Rather, we are monitoring market volatility and ensuring portfolios remain diversified and appropriately balanced. Portfolio diversification is one of the key risk management tools we employ, and this is evidenced by our diversification not only across asset classes such as stocks, fixed income, and alternative investments, but also across geographies like the U.S., Developed International Markets, and Emerging Markets. In 2020, the U.S. was home to a little more than 4% of the world’s population[5] and contributed nearly 24% of global GDP.[6] However, the latter has gradually declined from 40% of global GDP in 1960,[7] a trend we don’t believe is likely to reverse in the coming decades. This is a key reason we maintain a meaningful exposure to non-U.S. markets.

Markets, economies, and societies are resilient, and when we consider intermediate- to long-term prospects we remain optimistic that growth, innovation, and collaboration will continue to solve the most pressing problems we face. In the meantime, we believe patience and a disciplined investment plan grounded in risk management will serve investors well during this challenging period.

All of us at Sapient thank you for allowing us to serve you, and we continue to work tirelessly to warrant the trust you have placed in us.

Sources:

1. NCB News, March 2, 2022 https://www.nbcnews.com/news/world/russia-attacks-ukraine-cities-kharkiv-biden-putin-pay-invasion-rcna18243

2. The Economist, March 9, 2022 https://www.economist.com/graphic-detail/2022/03/08/russias-reliance-on-energy-spells-trouble-for-its-economy

3. Trading Economics, Citing 2020 Date from the World Bank https://tradingeconomics.com/russia/gdp

4. Bespoke Investment Group, “Market Reaction to Major Geopolitical Conflicts Since 1940,” February 2022

5. Worldometer, Citing 2020 data from the United Nations https://ycharts.com/indicators/us_gdp_as_a_percentage_of_world_gdp

6. YCharts, Citing 2020 Data from the World Bank https://www.worldometers.info/world-population/us-population/

7. Visual Capitalist, January 14, 2021 https://www.visualcapitalist.com/u-s-share-of-global-economy-over-time/

Although the statements of fact and data in this report have been obtained from, and are based upon, sources that the firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed. All opinions included in this report constitutes the Firm’s judgment as of the date of this report and are subject to change without notice. This report is for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Past performance is not a guarantee of future results. Indexes, such as the S&P 500 Index, are not directly investable.